Unisys Corporation (NYSE:UIS) recently delivered better than expected EPS, quarterly net sales, and beneficial guidance. In addition, management is investing in growing target markets like the global digital workplace market, and is developing new products with AI and machine learning features. I also appreciate the recently reported cost-reduction initiatives, and would expect FCF growth thanks to recurring revenue. There are obvious risks from postretirement liabilities and the total amount of debt, however UIS does, right now, trade quite undervalued.

Unisys: Has Recurring Revenue, And Operates In Growing Markets

Founded in 1986 in the United States, Unisys is an information technology solutions company with global reach. With a significant amount of know-how accumulated, Unisys’ solutions and services are offered through global distribution platforms that allow it to carry out large-scale projects.

The company’s clients are in the public and private sectors, primarily including state and local governments and agencies as well as global non-profit organizations. Its business customers, on the other hand, are diversified across various sectors. Some of the company’s industrial and business process computing solutions have a more concentrated customer base, especially in areas such as travel and transportation.

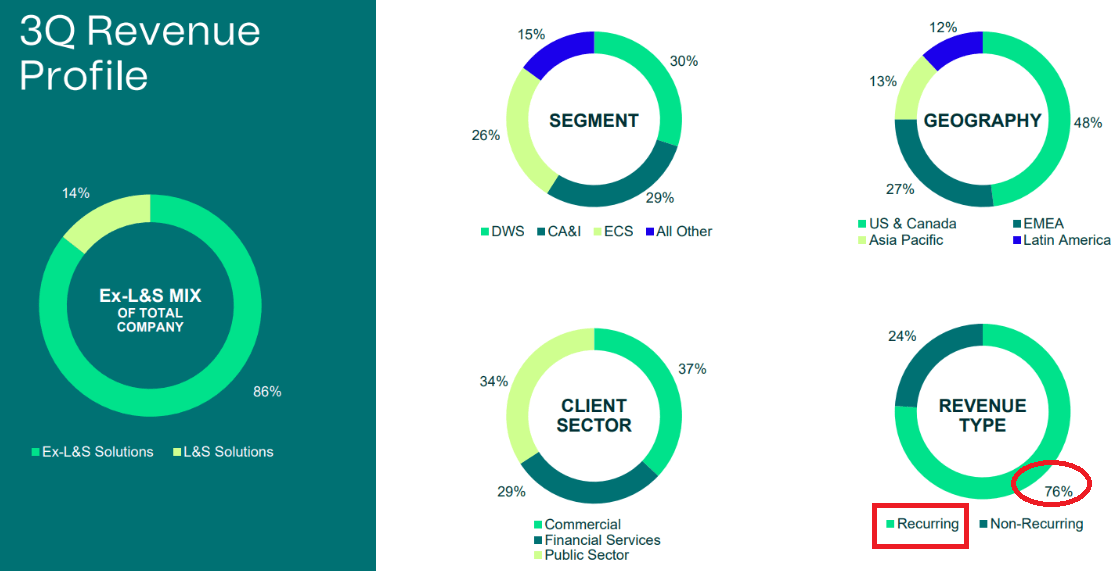

The company’s revenue is also geographically diversified as Unisys reports revenue in the United States, Canada, EMEA, and Asia Pacific. Having said so, I believe that the most appealing is the amount of recurring revenue. In the last quarter, 76% of the total amount of revenue was recurring. With that level of recurring revenue, I think that future net sales will most likely exhibit more stability than that of peers. The following is a slide from a recent presentation.

Source: Quarterly Presentation

The company has three reportable segments: Digital Workplace Solutions, Cloud, Applications and Infrastructure Solutions, and Enterprise Computing Solutions. The first of these segments focuses on the workspace design operations. It provides advice, and carries out the implementation and integration of business technologies for data-driven management and other applications.

The segment Cloud, Applications and Infrastructure Solutions is responsible for accelerating digital transformation in critical areas such as cloud migration and management in addition to application and infrastructure modernization. Its solutions accelerate hybrid and multi-cloud adoption. and help its customers leverage the flexibility and efficiency of the cloud to drive business growth. The Enterprise Computing Solutions segment offers high-intensity software-defined solutions in the cloud and on-premises. The biggest business is optimizing computing architectures as part of the digital transformation in various industries.

Revising the target market growth for Unisys Corporation is not easy because the company has several business segments. However, I believe that the company operates in markets that grow at a significant pace. The global digital workplace market, for instance, is expected to grow at close to 22% from 2022 to 2030. I believe that market growth will most likely enhance the net sales growth of Unisys Corporation in the coming years.

The global digital workplace market size was valued at USD 27.33 billion in 2021 and is expected to expand at a compound annual growth rate of 22.3% from 2022 to 2030. Source: Digital Workplace Market Size

Guidance Improvement, And Better EPS Than Expected

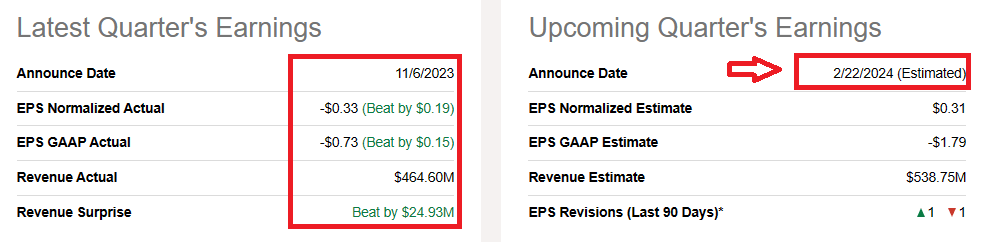

Unisys recently noted better than expected EPS and better than expected net sales. EPS was close to -$0.73, and the quarterly report was equal to $464 million. Considering the recent momentum in earnings, I think that we could see more earnings surprises in February 2024.

Source: SA

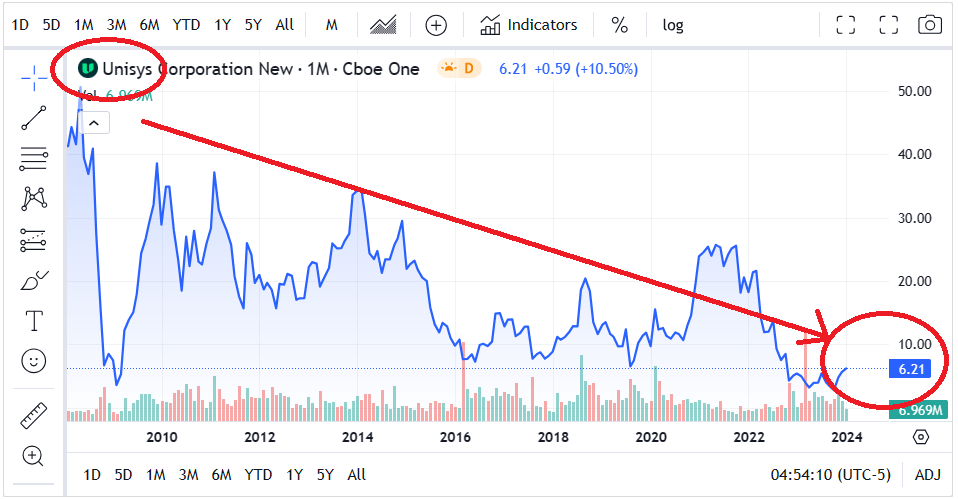

Unisys Corporation recently revised its guidance. 2023 Adjusted EBITDA margin increased to 12.5%-13.5%, and operating margin increased to 5%-6%, while revenue growth was revised to close to 1.5%. The company is currently trading at multi year lows, so I believe that the market did not really take into account the recent guidance improvements.

Source: Quarterly Presentation

Source: Ycharts

Stable Balance Sheet, But Shareholders Need To Take Into Account Postretirement Liabilities

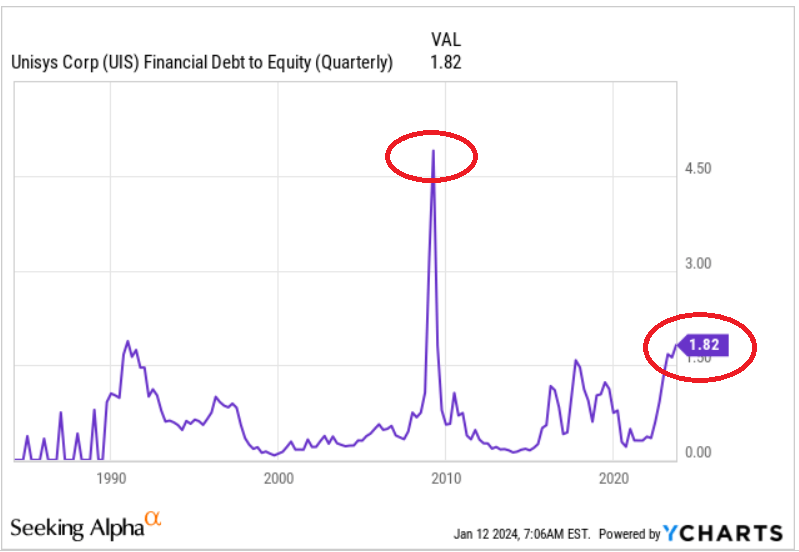

With a significant amount of cash in hand, the most valuable assets are represented by software, accounts receivable, and goodwill. These assets are financed with some debt and deferred revenue, and Unisys also reports some accounts payables. I am really not concerned about the total amount of debt, because Unisys noted larger financial debt/equity in 2010. However, I would understand that some investors dislike the total amount of leverage.

Source: Ycharts

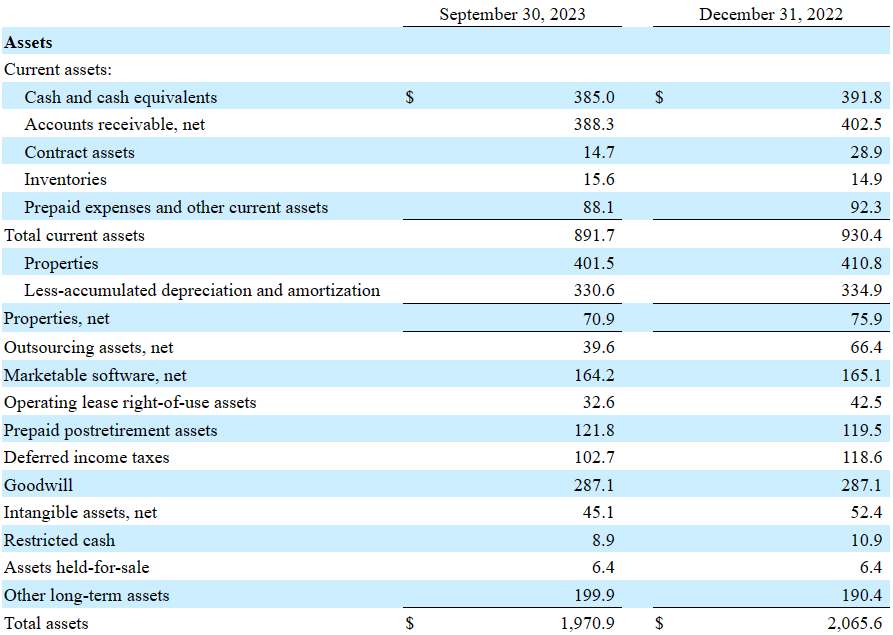

As of September 30, 2023, Unisys Corporation reported cash and cash equivalents worth $385 million, accounts receivable of $388.3 million, and total current assets of about $891.7 million. The current ratio is larger than 1x, so I think that liquidity does not seem a problem.

With properties worth $401.5 million and less-accumulated depreciation and amortization of about $330.6 million, the company also noted marketable software worth $164.2 million. In sum, right now, the software is worth more than the net properties owned. The company also noted goodwill of about $287.1 million, intangible assets worth $45.1 million, and total assets of about $1.970 billion. The asset/liability ratio is more than 1x.

Source: 10-Q

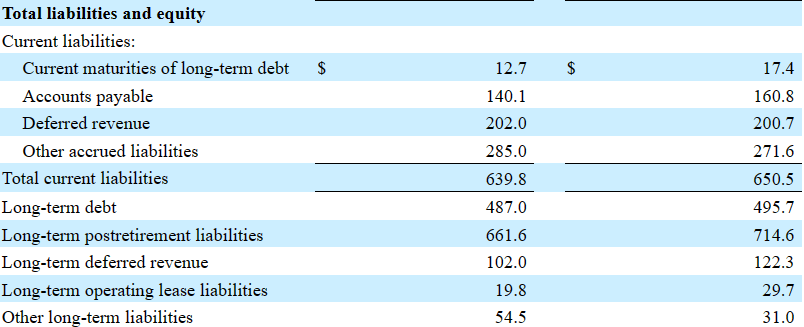

Investors may also want to take into account the long-term postretirement liabilities, which are not small. In the most recent months, we have seen a reduction in the postretirement liabilities. I believe that further reduction would most likely lead to higher EV/FCF and EV/EBITDA multiples.

Current maturities of long-term debt stand at close to $12.7 million, with accounts payable of about $140.1 million, deferred revenue worth $202 million, long-term debt close to $487 million, and long-term postretirement liabilities of $661.6 million.

Source: 10-Q

I Believe That New Developments In AI And Machine Learning Could Lead To Net Sales Growth

Unisys is currently developing applications of artificial intelligence, machine learning, hyper-automation, and quantum computing and encryption among other areas. I believe that further investments in such types of value-added products could bring cross-sell and upsell opportunities with its existing customers. In this regard, I think that it is worth mentioning that the company notes 455 active patents in the United States.

Further Relationships With Resellers And Alliance Partners Will Most Likely Lead To Net Sales Growth

The company also has a direct sales force that is complemented by resellers, alliance partners, and distributors abroad. Some of the company’s development focuses are on solutions associated with hybrid work, multi-cloud implementations, integration of numerous massive data sources, process automation, and cybersecurity. In my view, further relationships with external partners could bring not only net sales growth, but also improvements in FCF margin growth. Given the know-how accumulated through the years, I think that Unisys has a lot to offer to new software vendors and other types of resellers.

Recent Cost-reduction Initiatives Noted In The Last Quarter Could Lead To FCF Margin Improvements

I believe that recent cost-reduction charges noted in the last quarter could have a beneficial effect on future cash flow statements. As a result, I believe that we could expect some improvement in the FCF margin and FCF growth. Additionally, as soon as more investors have a look at the efforts of Unisys, the stock demand may increase.

During the nine months ended September 30, 2023, the company recognized net cost-reduction charges and other costs of $5.3 million. The net charges related to work-force reductions were $4.4 million, principally related to severance costs. Source: 10-Q

Unisys Corporation Is Offering More Solutions To Existing Clients, Which May Lead To Further Net Sales Growth

In the last quarters, two of Unisys’ business segments included net sales growth thanks to new scope with existing clients. I believe that research and development efforts and further investments in sales and marketing are definitely helping Unisys to offer more solutions to clients. As a result, thanks to further R&D expenses, sales, and marketing, I think that we could expect further increases in net sales growth in the coming years.

DWS revenue was $140.9 million for the three months ended September 30, 2023, an increase of 8.3% compared with the three months ended September 30, 2022. The increase in revenue was primarily driven by additional scope with existing clients. Source: 10-Q

CA&I revenue was $133.5 million for the three months ended September 30, 2023, an increase of 9.2% compared with the three months ended September 30, 2022. The increase in revenue was due in part to new scope with existing clients. Source: 10-Q

My Assumptions About Cost Of Capital Include A Conservative WACC Of 8.1%

In the last quarterly report and the last annual report, Unisys Corporation noted 6.875% senior secured notes due 2027. Given these figures, I believe that taking into account a WACC of 8.1% would make sense.

As of December 31, 2022, the company had outstanding $479.2 million of 6.875% senior secured notes due 2027. As the 2027 Notes have a fixed interest rate, the company does not have financial and economic exposure related to rising interest rates with respect to the 2027 Notes. However, the fair value of fixed rate instruments fluctuates when interest rates change. As of December 31, 2022, the fair value of the 2027 Notes was $373.0 million. Source: 10-k

Source: 10-k

Competitors: Unisys Appears To Be Trading Undervalued

The information and technology services industry is a highly competitive market that is affected by rapid changes in technical advances. Its main competitors are systems integrators, consulting and other professional services firms, outsourcing providers, infrastructure service providers, computer hardware manufacturers, and software providers. I believe that Unisys’ investment in proprietary developments through partnerships and other strategies along with investment in its commercialization capabilities will most likely have a favorable impact on its competitive position.

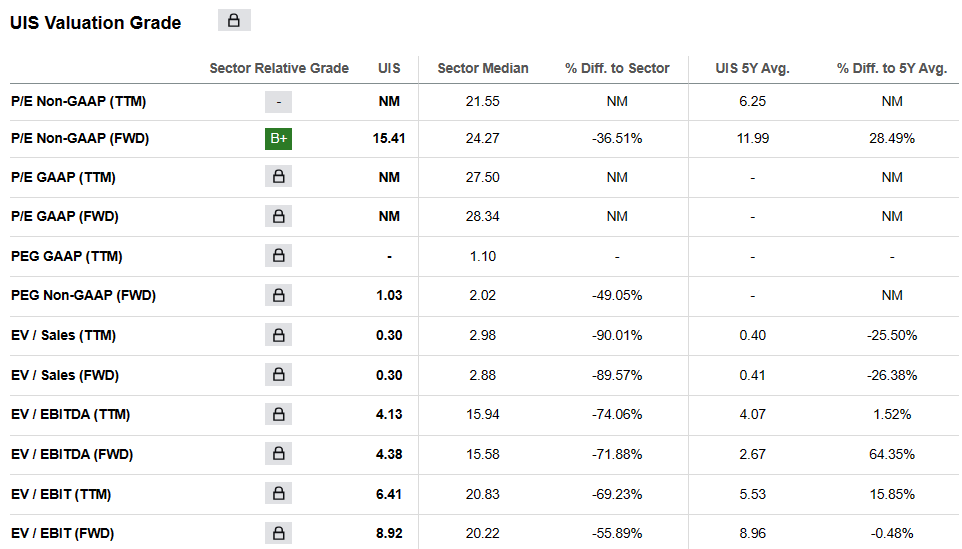

Given this information about the industry and noting Unisys’ significant know-how accumulated, I do not understand the current rating multiples. Peers are trading at close to 15x EBITDA, which is significantly lower than Unisys’ multiple. The sector median PE ratio is also significantly lower than that of Unisys. With these figures, I assumed a trading multiple of 9x FCF, which I believe is conservative.

Source: SA

DCF Model

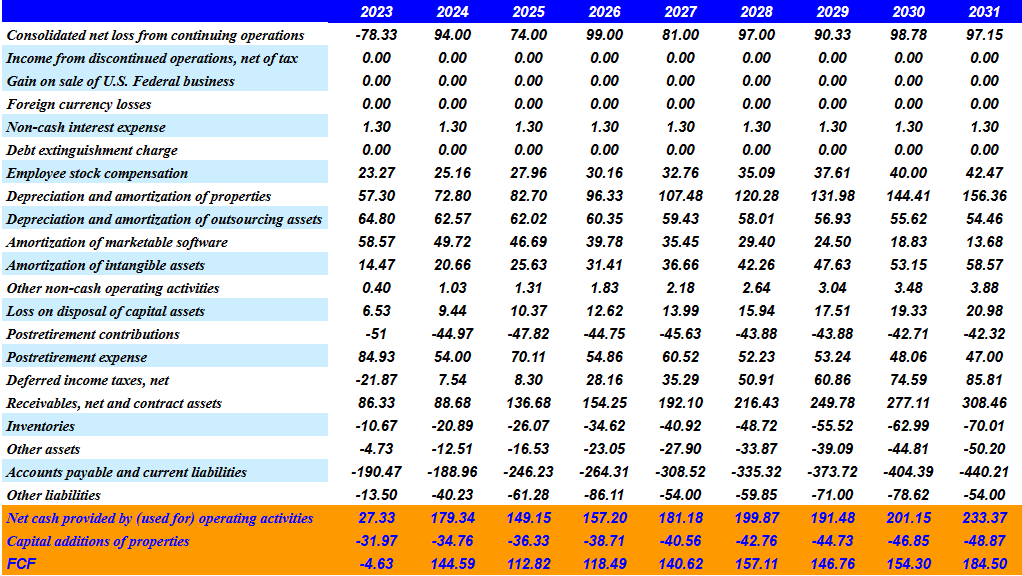

My cash flow expectations include 2031 consolidated net income from continuing operations of close to $97 million, employee stock compensation of close to $42 million, 2031 depreciation and amortization of properties worth $156 million, and depreciation and amortization of outsourcing assets worth $54 million.

My cash flow expectations also include 2031 amortization of marketable software of about $13 million, amortization of intangible assets worth $58 million, postretirement contributions of -$43 million, postretirement expense worth close to $47 million, and receivables of $308 million.

Additionally, with changes in inventories of about -$71 million and changes in accounts payable and current liabilities of about -$441 million, I obtained net cash provided by operating activities worth $233 million. Finally, with capital additions of properties of -$49 million, I obtained 2031 FCF of $184 million.

Source: My Cash Flow Expectations

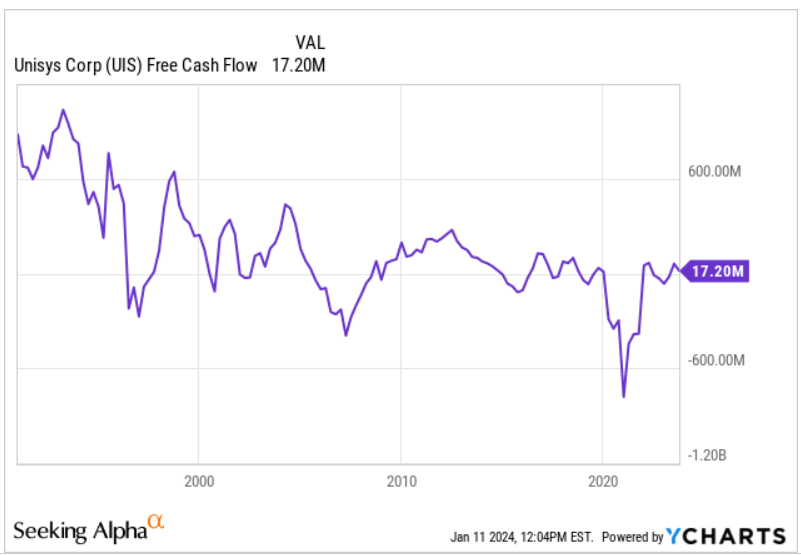

Unisys Corporation reported FCF of more than $600 million in the past, so I believe that my FCF figures, which do not exceed $200 million, seem conservative.

Source: Ycharts

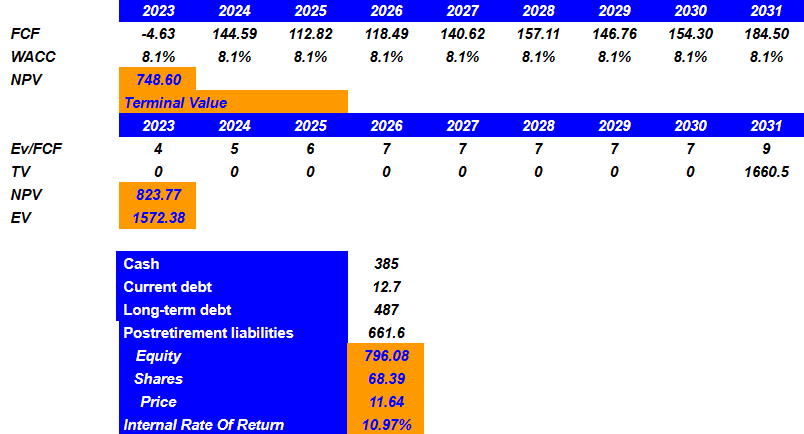

Under my DCF model, with a WACC of 8.1% and conservative free cash flow from 2023 to 2031, I obtained a net present value of future FCF of $748 million. In addition, with an EV/FCF exit multiple of 9x, I obtained a NPV of the terminal value of $823 million. The enterprise value stands at $1.57 billion, the implied equity would be $796 million, and my forecast price would stand at $11 per share. Finally, the internal rate of return would stand at 10.97%.

Source: My Cash Flow Expectations

Risks

The technology industry is one of the most competitive, and is characterized by evolving standards, predominantly short product life cycles, and continually changing demand patterns. Hence, I believe that discoveries and innovations that may emerge in the sector could unforeseeably affect Unisys’ future net sales growth.

It is also worth noting that Unisys delivered lower net sales growth than some competitors, and net income was also negative in the past. I do believe that the company is investing in promising technological sectors. However, demand for the stock may not increase because of previous negative results.

With regard to the total amount of debt and postretirement liabilities, investors may need to keep in mind that these are obligations that Unisys may have to pay. As a result, without potential negotiation with employees, future FCF growth may be limited.

Conclusion

Currently developing products related to artificial intelligence or machine learning as well as operating in growing markets, Unisys could bring net sales growth soon. The quarterly EPS and net sales were better than expected, and 2023 guidance was beneficial. These are promising points about Unisys. Additionally, with recent cost-reduction initiatives and quarterly net sales growth in two business segments, Unisys may soon trade at better price marks. There are some risks from the total amount of postretirement liabilities and debt. However, I think that the current valuation appears too cheap.